Dismantling the MVR 4.3 Billion SOE Machine

The state has pumped MVR 4.3 billion into SOEs this year. It’s time to turn off the tap.

We need to talk about the budget. Not the one on paper, but the one playing out in reality.

At the start of this year, the narrative was clear: fiscal discipline. We were told that the government would tighten the belt on State-Owned Enterprises (SOEs). The budget allocated for capital contributions—money given to these companies just to keep them running or expanding—was set at a modest MVR 378.3 million.

It sounded like a plan. It sounded like reform.

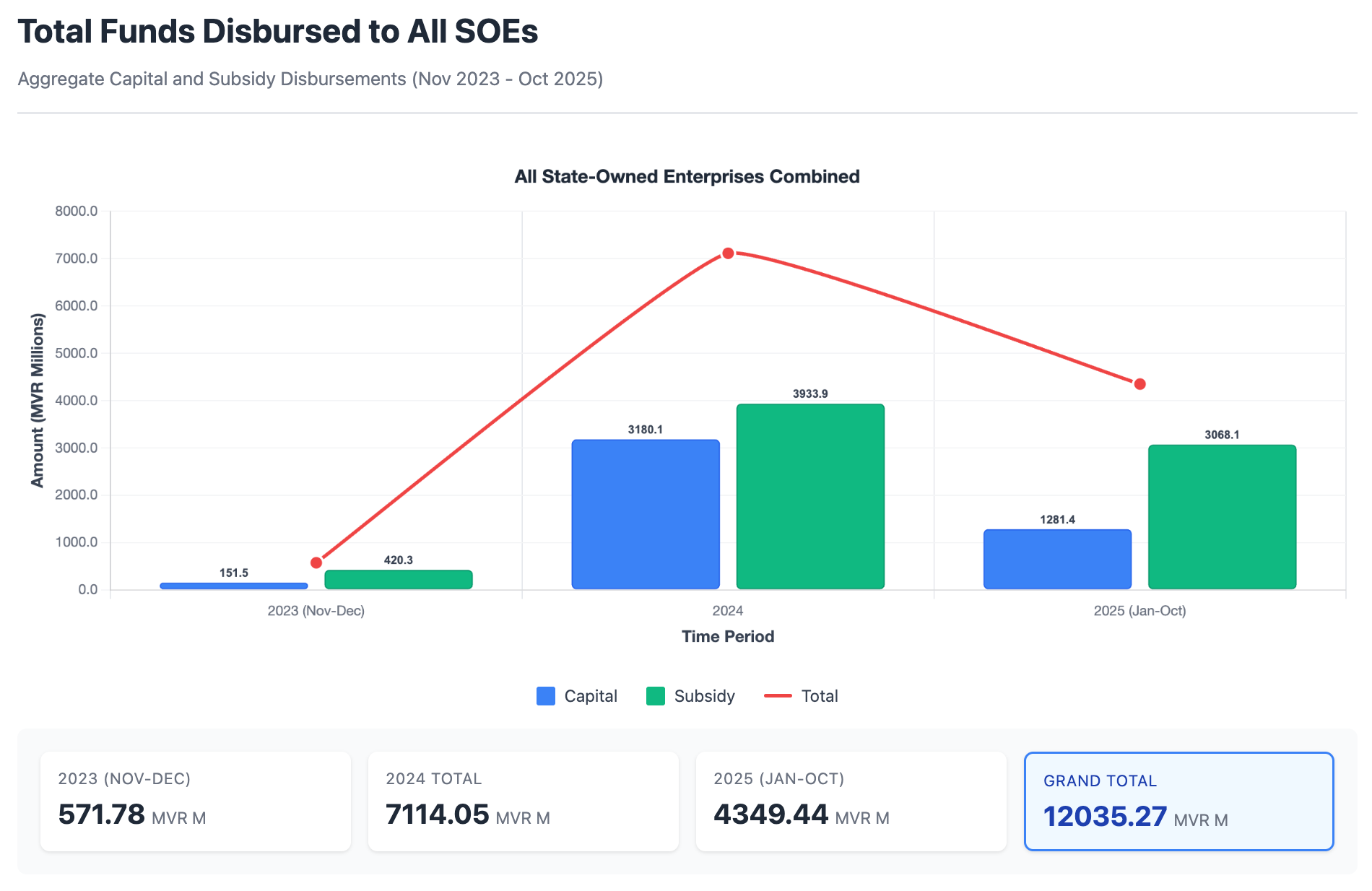

But as of October, that plan has evaporated. The government has already pumped MVR 2 billion into these companies as capital. That is not a typo. That is MVR 1.6 billion more than what was budgeted.

If you look at the same period last year, we have spent nearly MVR 287 million more this year. For all the talk of austerity and reform, the drain on the public purse is actually widening.

Where is the money going?

According to statistics obtained by Dhauru, we can see exactly where these injections are flowing. It isn’t going into innovation; it’s mostly going into keeping the lights on and the machinery moving in companies that struggle to stand on their own feet.

Just look at the top beneficiaries of this capital injection in the first six months:

Fahi Dhiriulhun Corporation (FDC): MVR 370.4 million

RDC: MVR 331.2 million

Fenaka: MVR 262.1 million

WAMCO: MVR 118 million

Addu Airports Company: MVR 62.3 million

But this MVR 2 billion is only half the story.

There is a second layer of spending hidden under “subsidies.” The government released another MVR 3.1 billion in subsidy grants to nine companies. The lion’s share, naturally, went to STO (MVR 1.8 billion) to suppress the price of staple foods and fuel.

When you do the math—combining the direct capital injections and the subsidies—the state has directly transferred MVR 4.3 billion to SOEs up until October.

The “Merger” Illusion

The government’s strategy so far has been consolidation. We hear about merging Company A with Company B, hoping that smashing two inefficiencies together will somehow create one efficiency.

But the numbers tell us this isn’t working. The goal was to reduce expenditure. The reality is a massive budget overrun. Mergers are often just administrative shuffling; they don’t solve the core rot of political patronage, bloated staffing, and lack of commercial discipline.

The Real Solution: Dismantle and Democratize

We cannot keep bailing out these companies with taxpayer money. It is unsustainable, and frankly, it is unfair to the private sector that has to compete without a government safety net.

We need a radical shift. We need to stop treating SOEs as extensions of the government and start treating them as businesses. And if they are businesses, let the market decide their worth.

My proposal is simple: List them.

We should be moving to list major SOEs on the Stock Exchange.

End the Dependency: If a company like Fenaka or RDC is viable, let it raise capital from investors, not the finance ministry.

Force Transparency: Publicly listed companies are subject to scrutiny that a government department is not. They have to answer to shareholders who care about profit and efficiency, not just ministers who care about votes.

True Ownership: Instead of “state ownership”—which really just means bureaucratic control—let Maldivian citizens own the shares.

The government needs to let go of the control. As long as the state holds the reins, these companies will always be treated as political tools rather than commercial entities. And as long as they are political tools, they will continue to cost us billions.

MVR 4.3 billion is a lot of money. It’s money that could have been spent on economic diversification or paying down our national debt. Instead, it was swallowed by the SOE machine.

It’s time to turn off the tap.