MMA's Quantitative Easing: A Risky Gamble

MMA is set to inject MVR 2.5B, but with usable reserves at just $189M, does it have the firepower to defend the Rufiyaa?

The Maldives Monetary Authority (MMA) is getting ready to launch a Quantitative Easing (QE) operation, marking a dramatic shift in monetary policy. The MMA is going to buy government T-bills from the Maldives Pension Administration Office for MVR 2.5 billion, or roughly USD 163 million.

The government’s justification appears to be straightforward: this action is meant to clear off the backlog of unpaid bills to the private sector and bring much-needed liquidity to the businesses.

A closer look at the figures, however, worries me.

The Looming Forex Challenge

The pressure on the Maldivian Rufiyaa, an unavoidable consequence of such a massive liquidity injection, is my main worry. The demand for US dollars will spike when the central bank pumps MVR 2.5 billion into circulation. The crucial question is whether the MMA has enough firepower to protect the value of MVR.

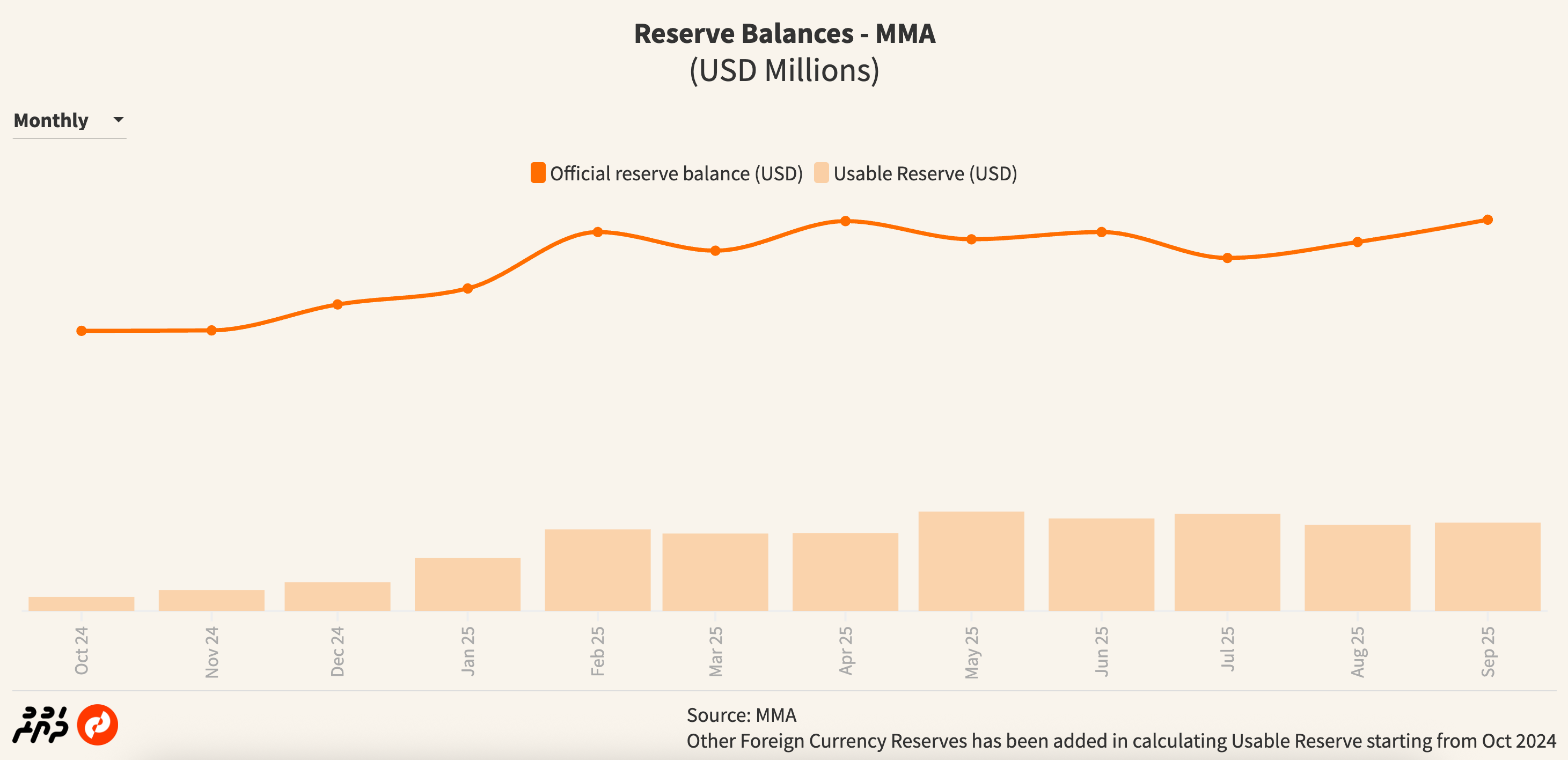

The reserve numbers are alarming. Since June, the MMA’s usable foreign reserves have been declining, and as of August, they were only USD 189 million. This indicates that our usable reserves are almost fully covered by the new injection of MVR 2.5 billion. This significantly limits the MMA’s ability to stabilise the currency by intervening in the forex market. Without a robust intervention mechanism, a depreciation of the Rufiyaa seems not just possible but probable.

Every household would be a hit. Higher import prices result from a weaker Rufiyaa, which directly contributes to inflation. An overheated economy could result from this, which would reduce purchasing power and put a heavy burden on common people.

A Puzzling Policy Reversal

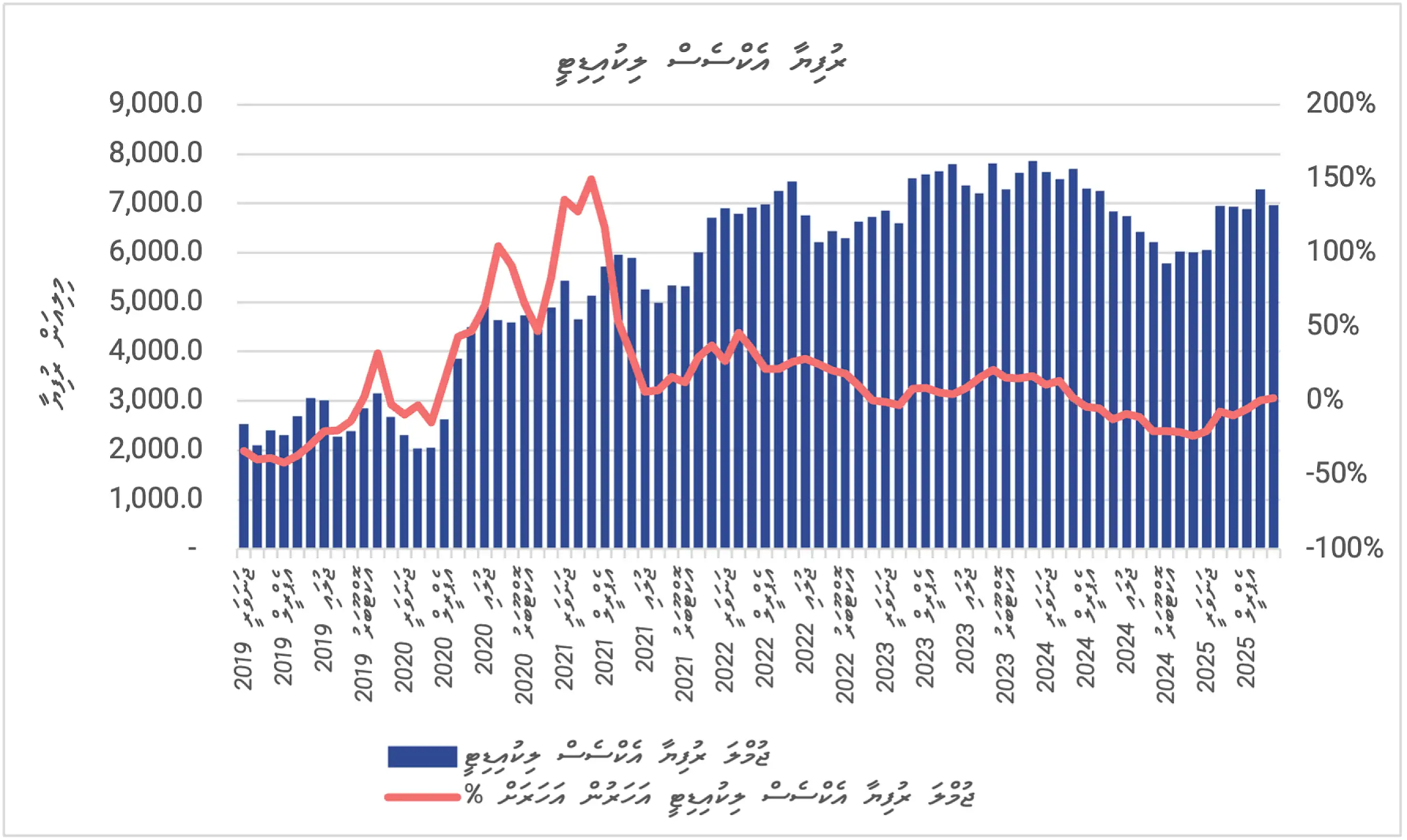

This move is especially confusing because of its timing and seeming inconsistency with recent policy. The MMA’s statistics show MVR 7 billion in excess liquidity in the circulation as recently as June. To address this, it rightly implemented a contractionary monetary policy, conducting Open Market Operations (OMO) to absorb the surplus Rufiyaa.

It seems inconsistent to now completely reverse policy and inject a significant amount of money into the economy. Why pivot from a policy designed for an economy with excess liquidity to one typically reserved for a liquidity crunch? This sharp reversal raises questions about the MMA’s underlying strategy and its reading of the economic reality.

This circumstance also draws attention to a deeper problem with governance. The MMA seems to be forced to finance the budget deficit as a result of the government’s inability to implement austerity measures. This sets a worrying precedent, blurring the lines between prudent monetary policy and fiscal support, which could compromise the central bank’s independence.

In my view the MMA must give a thorough and unambiguous explanation for this QE operation before moving forward. They must specify the precise actions they plan to take in order to:

Mitigate the immense pressure on the forex market.

Control the inflationary spiral that is likely to follow.

Prevent the economy from overheating.

This well-intentioned liquidity injection could quickly turn into a dangerous gamble with the country’s economic stability if there is no clear plan in place.